Reset!, Live DMA and the Syndicat des musiques actuelles have joined forces to map who owns what in the live music sector and call for policy action.

Behind many sold-out shows and energetic festivals, ownership structures remain invisible to audiences but play a decisive role in who operates stages, how risks are shared, and where revenue flows.

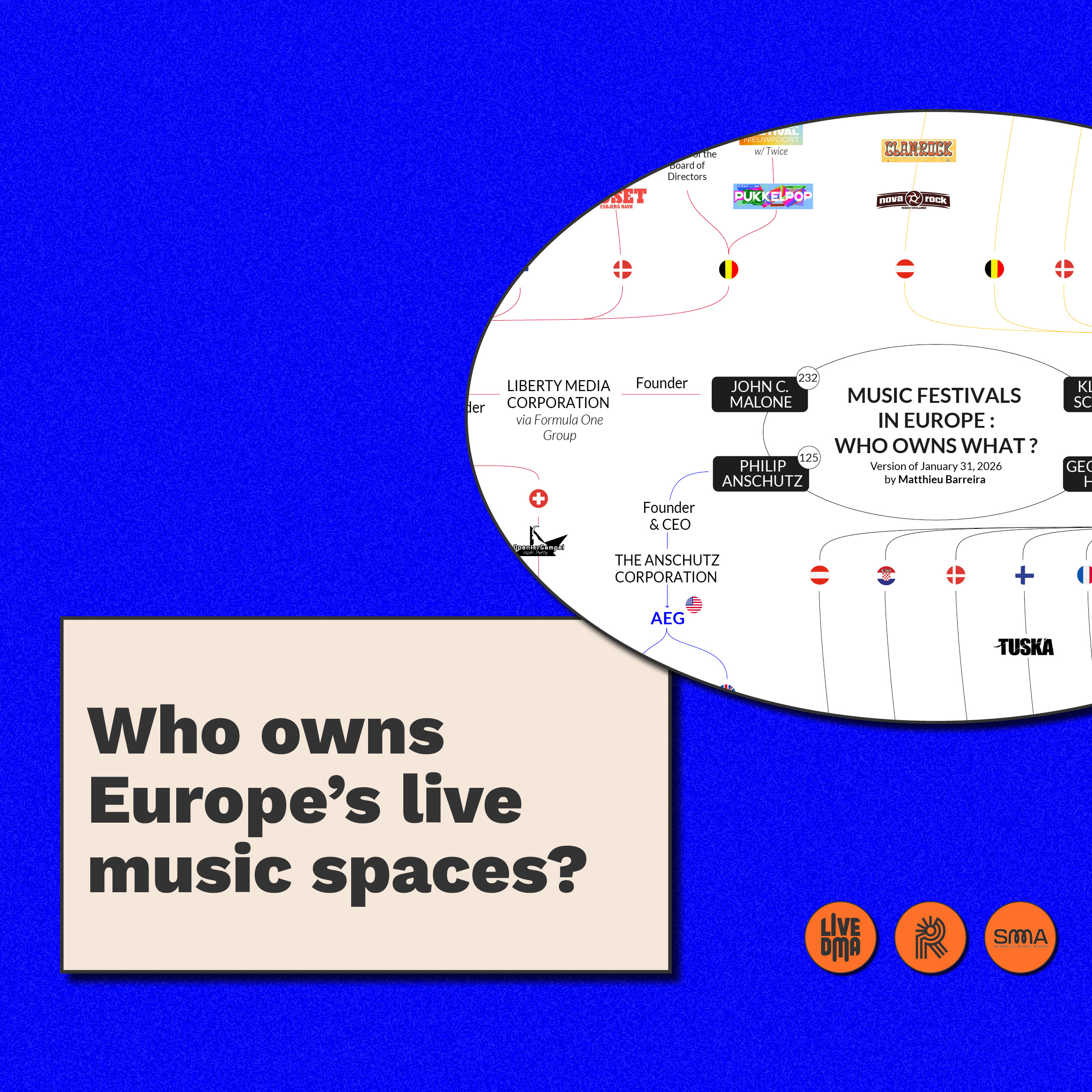

The new European ownership maps show that more than 150 of the largest festivals in the European Union are controlled by just four groups: Anschutz Entertainment Group (AEG), Live Nation, CTS Eventim, and Superstruct.

Superstruct, recently acquired by private equity firm KKR with CVC as co-investor, owns and operates more than 80 music festivals across ten countries in Europe and Australia, including Wacken Open Air, Tinderbox, Zwarte Cross, and Sónar.

Live Nation operates around 120 subsidiaries in the European Union and reported a turnover of about $16.7 billion in 2022. AEG Presents, the live events arm of Anschutz Entertainment Group, is described as the second biggest live music promoter in the world and combines concert promotion with ownership of major venues such as the O2 Arena in London and the Mercedes-Benz Arena in Berlin. CTS Eventim, one of the leading international providers of ticketing and live entertainment, generated €1.9 billion in sales in more than 20 countries in 2022 and operates ticketing portals such as eventim. de, oeticket.com, and ticketone.it, as well as arenas including Lanxess Arena in Cologne and the Waldbühne in Berlin. By comparison, the 2,280 music venues and clubs in Live DMA’s network generated a total income of €1.7 billion in 2019, corresponding to an average income of roughly €0.75 million per venue.

An earlier version of the map already documented how multinational groups had taken stakes in dozens of European festivals. The new European festival ownership map confirms this pattern and integrates the most recent changes, including the acquisition of Superstruct by KKR and CVC in 2024, and it shows a rapid expansion in our sample: between 2022 and 2025 the number of mapped festivals linked to Live Nation rose from 74 to 78, Superstruct from 34 to 63, CTS Eventim from 42 to 51, and AEG from 5 to 10—increases of roughly +9%, +82%, +19%, and +80% respectively. For venues, the picture is different but connected. The ownership maps show that the main targets for consolidation have so far been arenas and stadiums. Groups such as AEG, Live Nation, and CTS Eventim operate or hold stakes in some of Europe’s largest arenas and stadiums, often as part of wider real-estate or mixed-use developments. These infrastructures are central to the current boom in stadium and arena tours, which trade sources describe as the busiest period ever for global stadium activity (IQ Magazine, November 26th, 2025).

Ticketing is another important node in this configuration. Several of the major live groups also control or operate large ticketing platforms. Live Nation, for example, owns Ticketmaster, which is described in policy and market analyses as the world’s largest ticketing company. These same analyses highlight concerns about speculative resale, the treatment of highly demanded events, and the possible impact of concentrated ticketing platforms on access and diversity.

At the other end of the spectrum, most small and medium-sized music venues remain independent, associative, municipal, or locally owned (European Parliamentary Research Service, “The EU’s live music sector – market distortion, value chains and ecosystem diversity”). They are the places where new artists start performing, where niche and experimental scenes can exist, and where local communities access live music on a regular basis. They do this with very limited margins and under strong pressure from real-estate dynamics and rising operating and regulatory costs. These types of venues are often described as “incubators” for emerging artists, noting that they carry a large share of the artistic and financial risk at the beginning of careers.

Large corporate operators are also exposed to inflation, regulatory requirements, and changes in audience behaviour. The difference lies in the way value circulates: when artists move from clubs to the big festival and stadium circuit, most of the additional income generated at that later stage does not flow back to the small venues that supported them in their early years. In most countries, there is currently no structured mechanism for grassroots venues to capture part of the value they help create. This structural imbalance is a central concern of our statement and raises, in the longer term, the question of whether dedicated redistribution tools—such as ticket levies or other solidarity schemes—are needed to stabilise the base of the live music ecosystem

Taken together, the ownership maps and existing studies show that:

— a small number of transnational groups control a large part of the high-capacity festival and arena segment;

— these groups generate some of the highest revenues in the sector and, according to their official statements, are all experiencing strong growth; — thousands of locally rooted venues and smaller festivals operate on comparatively modest financial bases and under more fragile conditions;

— concentration appears at several levels of the live music chain, including festival ownership, venue operation, and ticketing (vertical and horizontal integration);

— the past three years have seen a significant number of buyouts and acquisitions, both within these groups and involving new entities. Many structures have disappeared, but others have emerged in their place;

— the fact that a group does not hold shares in a given structure does not mean that it has no direct or indirect influence over it, given these groups’ dominant positions in certain areas, such as programming, booking and sponsorship, or through their board positions;

— regarding venues and festivals exclusively, the phenomenon can be considered relatively minor (purely in terms of quantity) given their numbers, whether at national or regional scales. However, if we focus on the capacities they represent, the artists booked, or their revenues, the picture changes completely. As other studies have shown, this highlights that the live music market is structured as an oligopoly fringe.

The European Mapping Project on Ownership Concentration in Live Music aims to make visible who owns which stages and to situate this evidence within wider cultural and competition policy debates.

By putting these structures into public sight, it invites institutions, professionals, and citizens to ask a simple question: when we buy a ticket for a festival or a concert, who do we really support, and what kind of ecosystem do we want for live music in Europe?